The Road to Economic Recovery

Highlights

We believe:

- Record volatility, the quickest decline into bear market territory, and a record setting recovery rally highlight an extreme market and economic environment. Despite the record setting moves, the S&P 500 is relatively flat for the year

- The recession we are in will be the shortest on record. Monetary and fiscal policy cannot solve the root cause of the recession, which was the virus, but will help bridge the gap to make the recession shorter and less painful

- Presidential election year trends, including increased volatility, will appear as we get closer to November

- There will be opportunities to play the yield curve steepening trade in intermediate and longer-term maturities

- The fiscal situation and rising budget deficit are concerns, which present long-term structural problems

- The internal condition of the market has improved considerably; however, there are many risks in the current environment and now is not time to throw caution to the wind

Revisiting Our January Market Outlook

We came into the year with the economy on solid footing. Jobless claims were low, the unemployment rate was at a 50-year low, housing starts were hitting cycle highs, and global PMIs were turning higher. Things were looking good for remaining on trend growth since the financial crisis ended. It looked like we would make it into the 12th year of the economic expansion. We expected moderate returns with some volatility given normal election year trends. That all changed quickly. Nobody predicted a global pandemic that would land a crushing blow to both the global economy and markets.

Our year-end target for the S&P 500 was 3500. It actually got close in mid-February before the crisis. We have not altered that target, even though we have had record volatility, the quickest decline ever from new high into bear market territory, and now the fastest market recovery in history. Surprisingly, the 3500 year-end target is within reach once again. But in this environment, market volatility can strike at any time.

A Look at the Last Few Months

Taking a look at the markets, you can see the massive swings we have lived through over the past five months. At the lows for the year, equities were down in excess of 30% on average and only cash and U.S. Treasuries offered safe haven status. The rebound has been spectacular, driven by massive coordinated central bank and fiscal policy actions.

Remember the Underdog cartoon series that aired in the 1960s and 70s? Underdog would say, “There’s no need to fear, Underdog is here!” I think we now have a similar slogan for the Federal Reserve. It’s now “Have no fear, the Fed is here!” The Fed has embarked on a “leave no asset behind program.” They are buying everything they can — Treasuries, corporate debt, municipal bonds, bond ETFs, and they are dead set on keeping the train rolling and forcing investors out on the risk spectrum.

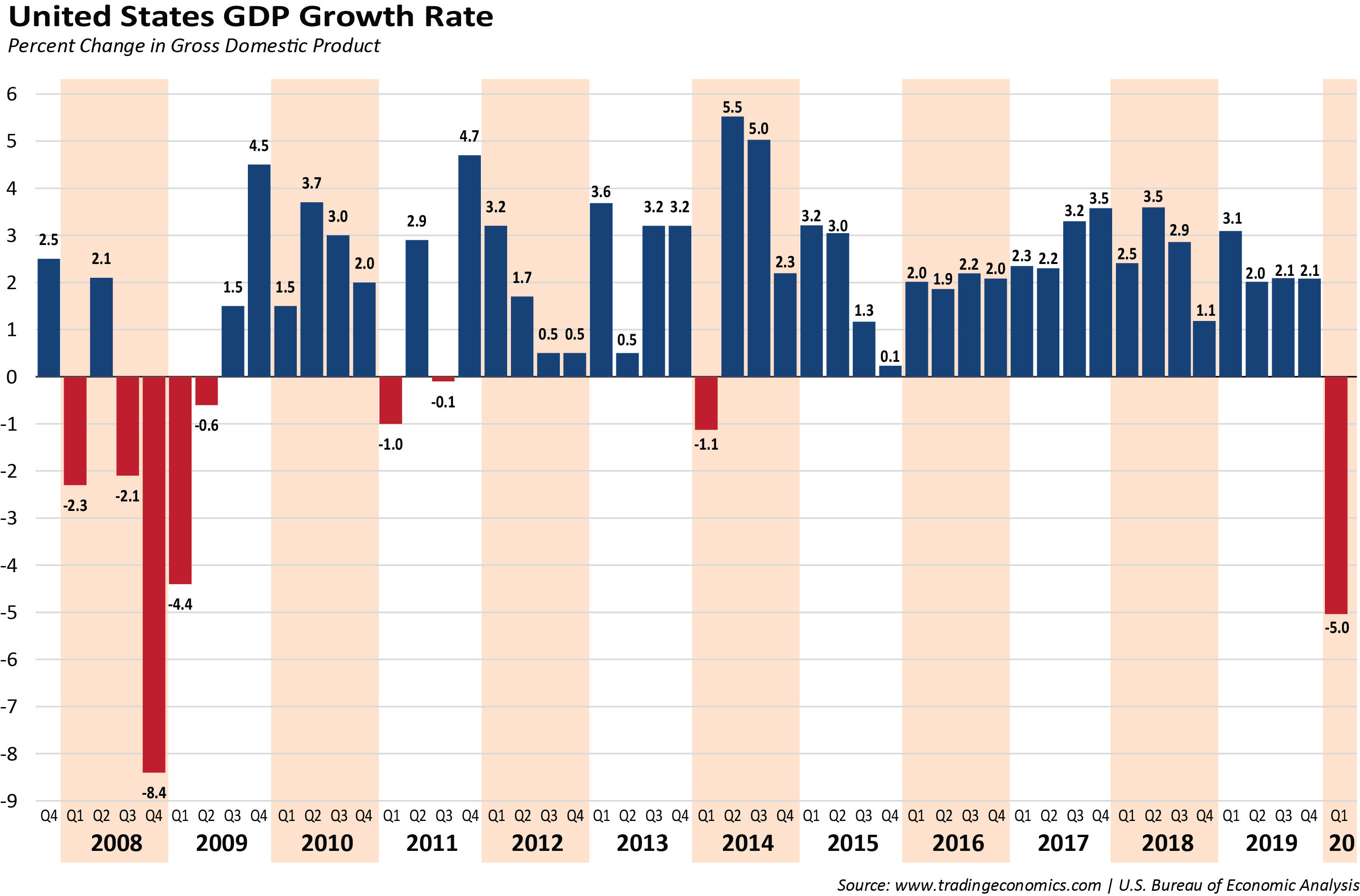

Figure 1. | United States GDP Growth Rates

A global recession and bear market took hold in March as governments around the world implemented social distancing and “shelter-in-place” restrictions to slow the spread of the COVID-19 pandemic. This is something that we have never seen before as it is a combination of a global health and economic crisis that led to a market liquidity crisis.

A global recession and bear market took hold in March as governments around the world implemented social distancing and “shelter-in-place” restrictions to slow the spread of the COVID-19 pandemic. This is something that we have never seen before as it is a combination of a global health and economic crisis that led to a market liquidity crisis.

Countries representing an estimated 92% of global GDP were placed under some form of social distancing. The economic consequences were devastating. The record long expansion in the U.S. ended with GDP contracting at a 5% annual rate in the first quarter. Second quarter GDP will be the worst on record. We expect GDP to contract by about -40% in the second quarter, in line with the Atlanta Fed GDPNow Forecast of a -45% decline. As we approach the end of the second quarter, the economy is improving as it reopens. We expect to see a sharp economic recovery in the third quarter with 20% growth, followed by 5% growth in the fourth quarter. There is much debate about the shape of the recovery: will it be a “V,” a “W,” or “U” shaped? We expect a sharp bounce back initially over the next two quarters and then a much slower pace similar to the trend growth we had during the previous expansion.

In our opinion, we are not likely to see the economy return to the peak levels of last February until late 2022 or early 2023. The Fed Chairman affirmed our expectations by saying the Committee expects to keep short-term interest rates near zero through 2022. Powell said, “We are strongly committed to using our tools to do whatever we can for as long as it takes.”

It’s official, the National Bureau of Economic Research (NBER), the group that dates the beginning and end of recessions, has declared that the recession started in March. That follows a record 128 months of expansion, in which the economy grew at a 2.3% annual rate, making it the slowest economic expansion on record. This was the fastest that the NBER has declared any recession since the group began formal announcements in 1979.

The Federal Reserve and Federal Government have stepped in massively to bridge the economic chasm we are facing. The Fed pulled out their entire game plan from the Financial Crisis and implemented it, and more, in a matter of weeks. We’ve also had several rounds of fiscal stimulus with more on the way. Most recently there is talk of a Cares 2 Act and a $1 Trillion infrastructure spending plan.

The recession we are currently in will likely be the shortest recession on record. An atypical duration might be expected with a one-of-a-kind downturn like this one, caused by executive orders to shut down the economy to help stem the spread of the virus.

The damage done on the employment front is staggering. Over 44 million people have filed for first time unemployment benefits in the last 13 weeks alone. To put this into perspective, job growth during the record long expansion following the Financial Crisis totaled 21.5 million people. In just the past three months, more people have been let go than were added to payrolls over the past almost 11 years.

Some Good News

There is a little good news; for example, the trends are improving, indicating that the worst of the crisis is behind us. Claims numbers have declined for 11 straight weeks as the economy reopens, and if the current trajectory remains intact, the weekly jobless claims number will be back to a more normal 400,000 weekly total in July.

In addition, nonfarm payrolls increased by 2.5 million in May and expectations are for an additional 3 million jobs to be added in June. The labor market has begun to heal, but nonetheless, we expect labor market slack to remain excessive for years, which will likely create downside pressure on wages and inflation.

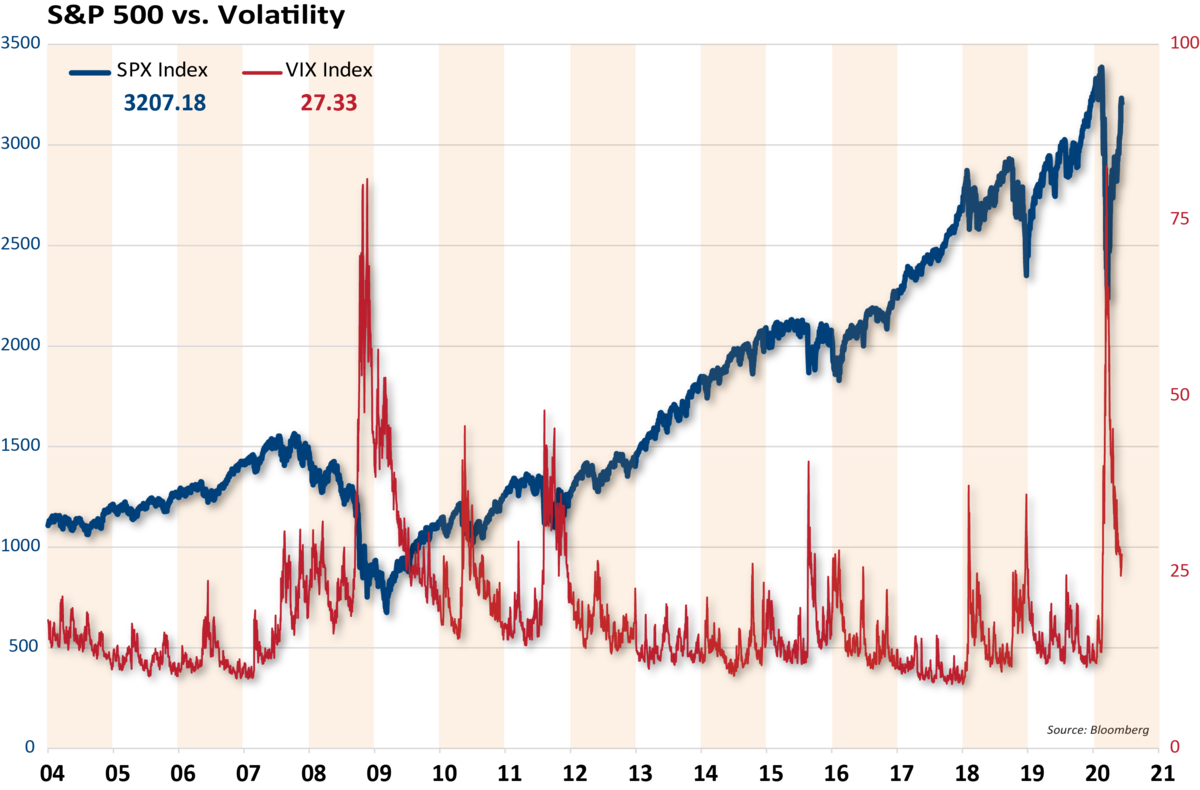

Figure 2: S&P 500 vs. Volatility

Unprecedented Volatility and the Shortest Bear Market on Record

Unprecedented Volatility and the Shortest Bear Market on Record

The preceding chart of the S&P 500 and the CBOE Volatility Index (VIX) illustrates the decline and subsequent quick rebound in stocks. In the midst of the decline, the S&P 500 plunged almost 34% in just 23 trading days.

It was the fastest ever decline from record high into bear market. Volatility spiked with the CBOE Volatility Index (VIX) hitting 82.69, its highest level ever. There was more panic selling than even during the Financial Crisis in 2008/2009.

To put this volatility event into perspective, in over 7,600 trading days since the VIX Index started, it has only closed above 80 three times, twice during the Financial Crisis in 2008 as well as on March 16th of this year. In addition, the S&P 500 peaked 84 days ago. In 58 of those days the S&P moved more than 1%. In 10 of those days it moved by 5% or more, and there was a period in mid-March with five consecutive trading days of 5% or greater moves. This has been an unprecedented volatility environment.

Since we had a full-fledged bear market as part of a collapsing economy, we thought it would be good to look at how this past bear market compares to others. It turns out that the bear we just had was the shortest on record of the 37 cyclical bear markets since 1900. On a percent decline basis, it was the 12th worst, or in the top one-third of all cyclical bear markets.

The 37% decline in the Dow Jones Industrial Average and 34% decline in the S&P 500 were slightly worse than the -30.9% average for all cyclical bear markets, but in line with the -34.6% average for cyclical bears associated with recessions.

Does this call into question the secular bull market theme? At this point we think the long-term bull market is still intact, given that it was the shortest cyclical bear on record. In addition, macro trends such as low interest rates, low inflation, and relative valuations of stocks compared to bonds still support the secular bull theme for now.

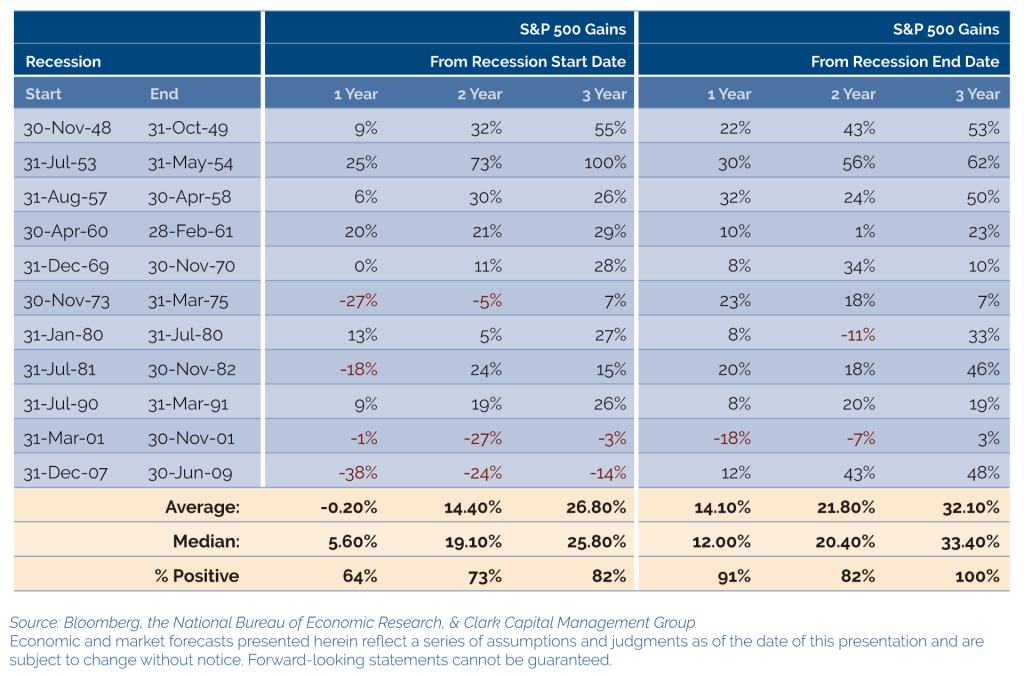

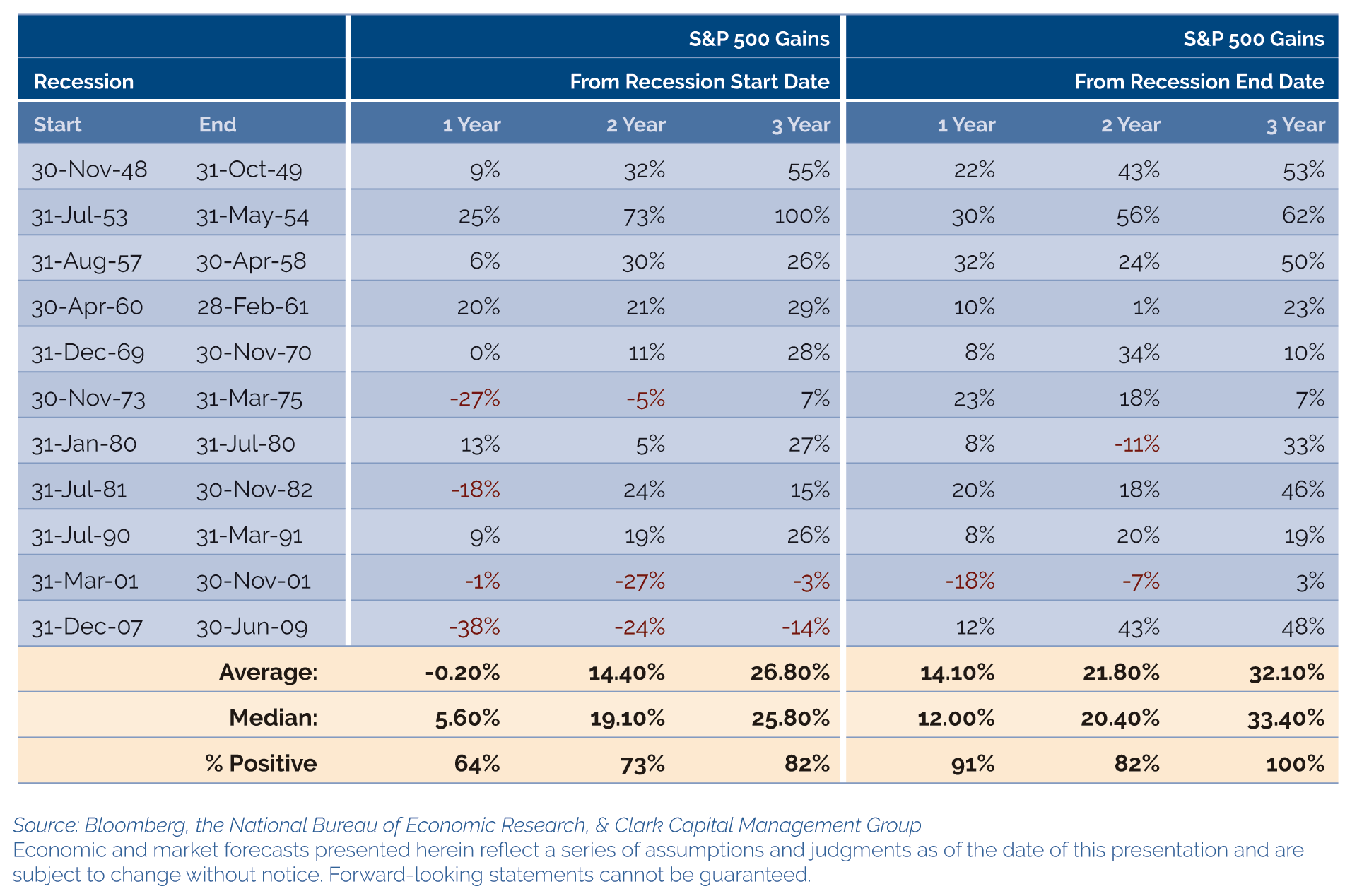

Figure 3. | How Have Stocks Done in Recessions

The Market’s Relationship to Recessions: Historical Perspective

The Market’s Relationship to Recessions: Historical Perspective

The National Bureau of Economic Research (NBER) is notoriously late in defining start and end dates to recessions. The dates are only known in hindsight. Even so, we can see by the data that the market actually doesn’t do too bad during recessionary environments. That is because the market is a discounting mechanism. It tops before recessions begin and bottoms before recessions end. On average, the market bottoms about four months prior to recession end date, which again is only known in hindsight. This time, the market bottomed earlier than average, and even before the NBER announced the recession start date.

From the start of recessions, the market has been flat on average one year later, and up 14% and 27% two and three years later respectively after recessions. The gains are even more impressive from the recession end dates, averaging 22% and 32% two and three years later respectively.

As far as relative performance after recession induced market lows, small-caps tend to outperform large-caps and cyclical value tends to outperform growth once the market bottoms. We are seeing both of these themes gaining traction currently.

Small-caps have outperformed large-caps by almost 1200 bps on average one year after the market bottom and by 900 bps one year after the recession end date. For cyclical value, a steepening yield curve, falling volatility, the start of a new bull market, and economic expansion normally provide a tailwind for relative outperformance following recessions.

The Markets and the Pandemic Remain Connected

Global confirmed cases of COVID-19 have increased to over 8 million people. In China, Beijing is clearly seeing cases rise in what may be a second wave of infections, and schools have been closed. In the U.S., testing continues to ramp higher as this chart shows, and daily tests are now consistently running at over 500,000. At the same time, the percent of tests coming back positive has been hovering around 5%, even as the number of tests rise. Also, the number of fatalities in the U.S. has continued to trend down, on average, since late April. In fact, the number of fatalities is now falling faster than the positive case count is falling, possibly indicating that a less vulnerable segment of the population is now being exposed. A word of caution, though, regarding the trends: states like Florida, Texas, Alabama, and Arizona are seeing rising case counts and more importantly, hospital utilization rates.

There are many signs that the economy bottomed in mid-April. The Apple Mobility Index bottomed in mid-April and is now at levels similar to January and February before the shutdown. Airline travel also clearly bottomed in mid-April, recently hitting its highest rate since pre-COVID. It certainly has a long way to go, and is still only at about one-fifth of last year’s demand.

Retail Sales rose by a record 17.7% in May, which was more than double the expectations and well more than double the next strongest month on record, which was October 2001. Manufacturing and service sector indices turned up in May, housing starts advanced for the first time in four months, and Leading Indicators turned higher in May. There are many green shoots appearing that suggest the worst of the economic decline is over. However, we expect it to be a long slog ahead.

Monetary and fiscal policy cannot solve the root cause of the recession, which was the virus. They can only help bridge the gap to make the recession shorter and less painful. Mission accomplished there, but it will take improved therapeutics and mass vaccination to solve the root cause.

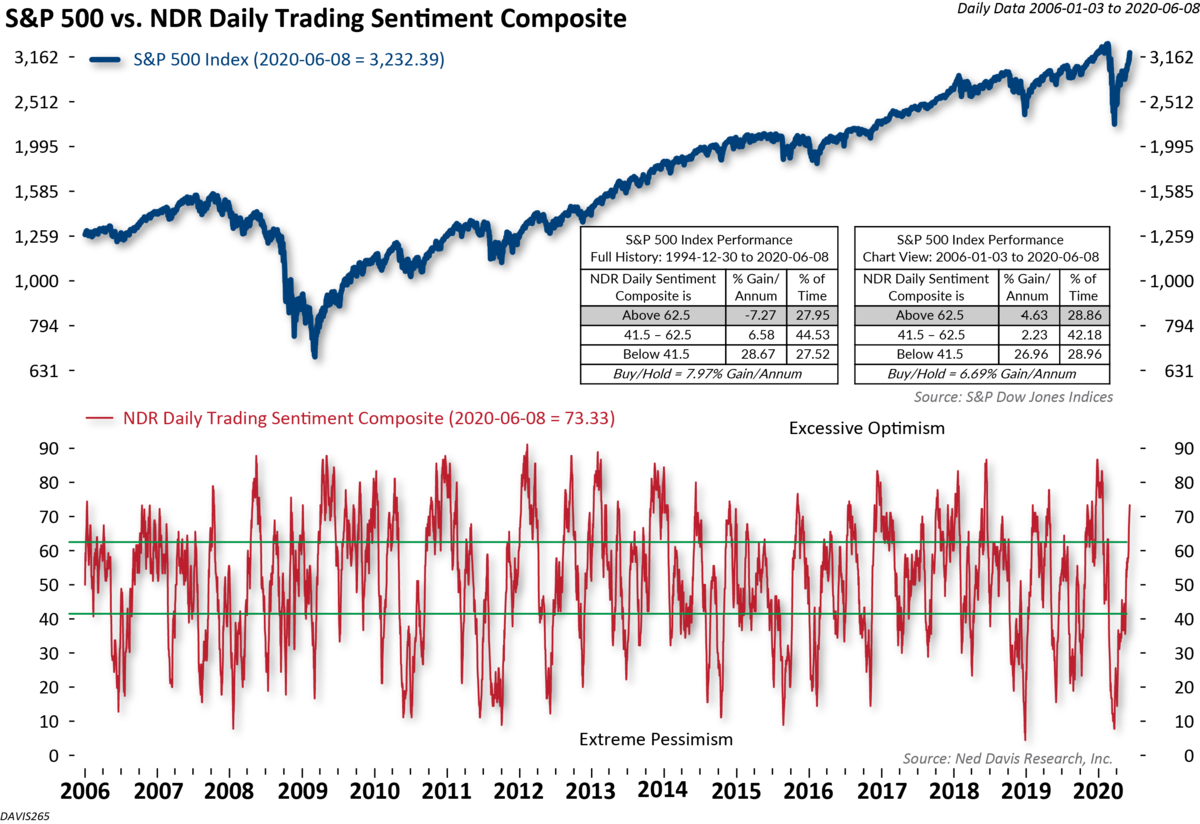

Investor Sentiment

Figure 4. | S&P 500 vs. NDR Daily Trading Sentiment Composite

Let’s turn to the markets, beginning with investor sentiment. Warren Buffet said, “Be fearful when others are greedy and greedy when others are fearful.” In our January 2020 Market Outlook we said “This short-term sentiment chart from Ned David Research shows that as the stock market has continued to hit new highs, investor sentiment has risen to an optimistic extreme. Extremes in investor sentiment are normally contrarian indicators, with optimistic sentiment leading to corrections or pullbacks, and pessimistic extremes leading to rebounds.” We have now done several round trips in sentiment. Investor sentiment hit one of its most pessimistic extremes in years at the March lows, and the 45% move higher in the S&P 500 has Investor sentiment now back into extreme optimism again.

In addition, put-call ratios, not shown here, sank to multi-year lows, also indicating a complacent environment. So, the market is likely due for a pause given the excessive sentiment readings.

Contrary to short-term sentiment statistics, longer-term sentiment remains favorable for the market. Fund flows out of equity funds and ETFs have been persistent while bonds have captured steady inflows. However, far too many investors make the same mistake over and over again. Fund flow data shows massive outflows from both equity and bond mutual funds and ETFs in March. In fact, flows out of bonds in the mid-March panic hit record extremes by a factor of four times. There was an historic selling of bonds.

Fund flows show what investors are actually doing, not just saying how they feel in sentiment surveys. As such, investors vote with their money, and by and large they have been selling stocks and buying bonds, except during the March panic. From a contrarian perspective, this does not indicate long-term equity market excesses.

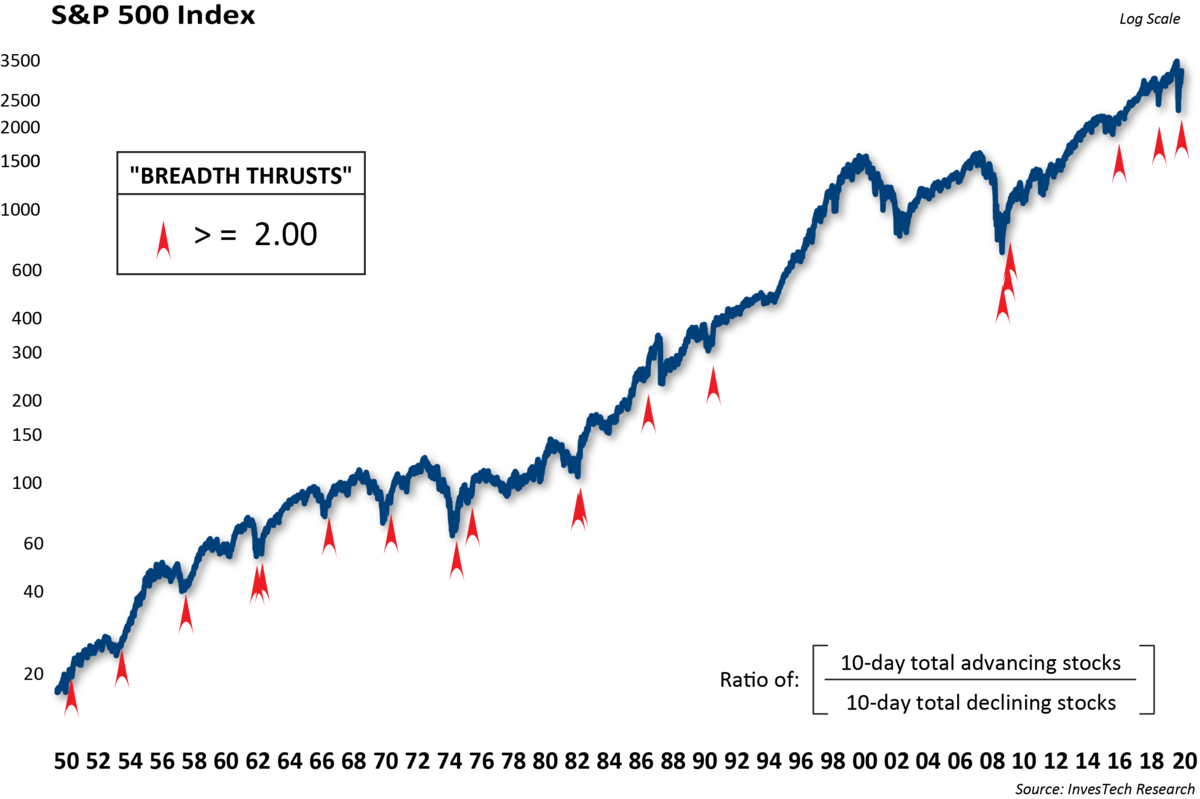

Short-term volatility notwithstanding, the internal condition of the market has improved considerably. Several breadth thrusts have registered including the number of stocks above their 50-day moving averages, the percent of stocks hitting new 20-day highs, and a surge in the 10-day advance/decline ratio. All of these breadth thrusts have a very good track record leading to gains over the intermediate term.

Figure 5. | S&P 500 Index

Another breadth thrust is when twice as many stocks are advancing compared to those declining over a 10-day period. This signal is rare and, according to InvesTech Research, typically appears at the beginning of a bull market or new bull market leg.

There have been two 10-day thrusts in the past ten years. The first appeared in July 2016 and the second in January 2019. The long-term track record is impressive, as none of the 18 signals since 1950 have resulted in a loss in the following six months.

In addition, off the lows on March 23rd the market had its strongest 50-day move in the S&P 500 since 1952, when the US stock market went to the five-day trading week. The S&P 500 gained 40% in just 50 trading days. There have only been two prior times with 50-day moves of 30% or better, and those came in October 1982 and May 2009. You may all know those dates pretty well. Both of those massive spikes turned out to be just the early innings of multi-year bull markets.

While this is clearly a good sign of strong momentum, there are many risks in the current environment so we wouldn’t throw caution to the wind.

Figure 6. | Dow Industrials Four-Year Presidential Cycle

Prepare for Presidential Election Year Trends

We thought a key factor for the market coming into 2020 would be the Presidential Election. That hasn’t been the case yet, but as we get closer to November, we suspect we will begin to see normal election volatility. While the outcome is uncertain, we have gone back and studied prior election years to glean hints as to how the market may respond.

In the post WWII era, the S&P 500 has averaged a 6.7% price gain in the election year, with gains 82% of the time. However, that doesn’t paint the whole picture. Uncertainty heading into presidential election has often been a headwind for stocks. The market normally corrects and consolidates in choppy trading during the primary season. It did so this year for different reasons. Although the election year rally has on average begun in May, the timing of the rally has varied widely, depending on when the market gets comfortable and discounts the eventual likely winner. When the incumbent party candidate has lost, however, equities have tended to decline into Election Day. After the uncertainty has passed, the market has historically rallied strongly into year end and well into the next year.

The market has tended to do better when the incumbent Republican wins. For example, in the post WWII era, there have been five cases of an incumbent Republican winning re-election, the S&P 500 has gained 8.2% in those years compared to declining 4.5% in the four cases when the incumbent Republican has lost.

President Trump had staked his presidency on the economy; the question is whether voters blame him for the recession or credit him for guiding the economy through the crisis. Currently, Joe Biden has about a 10-point lead in national polls. This election is a wild card due to the recession and virus. However, looking at history, it is very rare for a President to win re-election in a recessionary year.

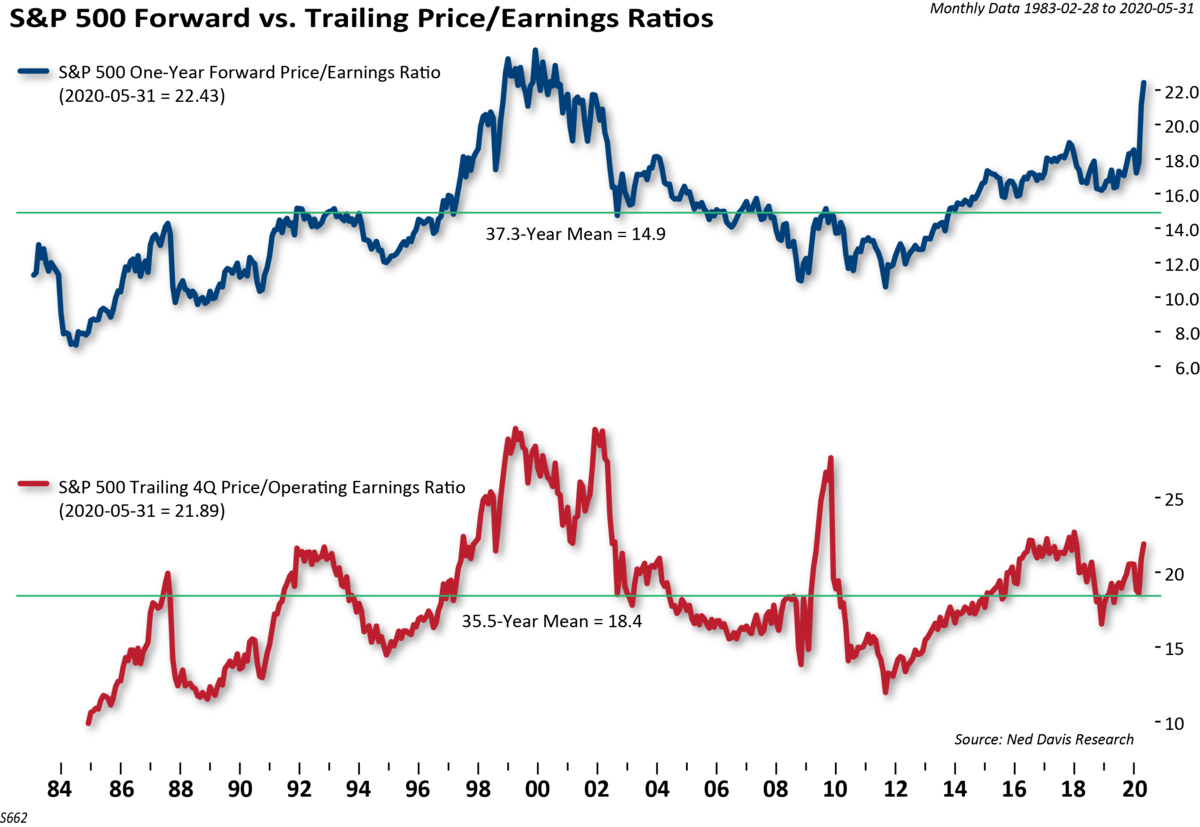

Figure 7. | S&P 500 Forward vs. Trailing Price/Earnings Ratios

Valuations: Stocks Still Not Cheap

Turning to valuations, stocks are not cheap when looking at P/E multiples. In 2019, we saw huge multiple expansion with the P/E ratios surging as prices rose much faster than earnings. This is fairly common coming off of a major market bottom.

The forward P/E for the S&P 500 is now the highest in nearly 20 years. That is from the sharp rebound in stocks at the same time earnings estimates have crumbled. The market is forward looking and looking beyond the economic and earnings chasm this year and into 2021. In order to support the lofty valuations, earnings growth will have to materialize moving forward.

We have said before that valuations can and have remained stretched for extended periods, so they are not timing tools, but more a measure to assess potential risks. The valuation landscape is a risk that we are monitoring.

Earnings estimates have plunged, with analysts now looking for a 30% decline in earnings for the year. Those estimates are front loaded with a record decline in the first half of the year.

If the economic rebound does prove to be slow, there could be downside risks to the Q4 2020 numbers, which are only at a -8.4% year over year decline. Investors are turning their attention to 2021 numbers. Consensus is calling for a 47% rebound in S&P 500 operating EPS next year. That would take earnings to a new record high.

Given the lofty valuations, plunging earnings, and sharp rebound in stocks, it appears the market is counting on earnings growth to come through in 2021. That does pose a potential risk if growth disappoints.

Figure 8. | S&P 500 Earnings Yield vs. 10-Year Treasury Yield

Looking at valuations from a different perspective, it’s important to recognize that low interest rates support higher valuations. With interest rates at record low levels, the relatively high valuation of stocks looks more realistic than it would during a period of much higher interest rates.

Here we have the earnings yield of the S&P 500 (the inverse of the P/E multiple) and the yield on the 10-year Treasury Note. By this measure, stocks are undervalued relative to Treasuries.

While it isn’t unusual for stocks’ earnings yields to run below corporate bond yields or Treasury yields, since 2009 there has been a persistent premium, and that premium has increased in recent months as interest rates have fallen to record lows.

The U.S. 10-year Treasury hit an all-time low yield of 0.38% on March 9th. That could very well be the low in yields, but they’re not likely to move up with the Fed’s asset purchase program in full swing. Yields could be in a trading range for a while, defined by 0.38% – 1.25% on the 10-year Treasury Note.

Actions of the Fed, the ECB, the BoJ, and others Central Banks suggest that they will keep their policy rates at the effective lower bound for a very long time. For example, there have been almost 200 central bank rate cuts that have led to Global Short Rates being more than cut in half! The short end will be well anchored near zero into 2022.

However, if we are on the economic upturn, history shows the yield curve has steepened after every economic recession during the following recovery. In our opinion, there will be opportunities to play the yield curve steepening trade, in intermediate and longer-term maturities.

The Fed, Debt Burden, and Inflation Expectations

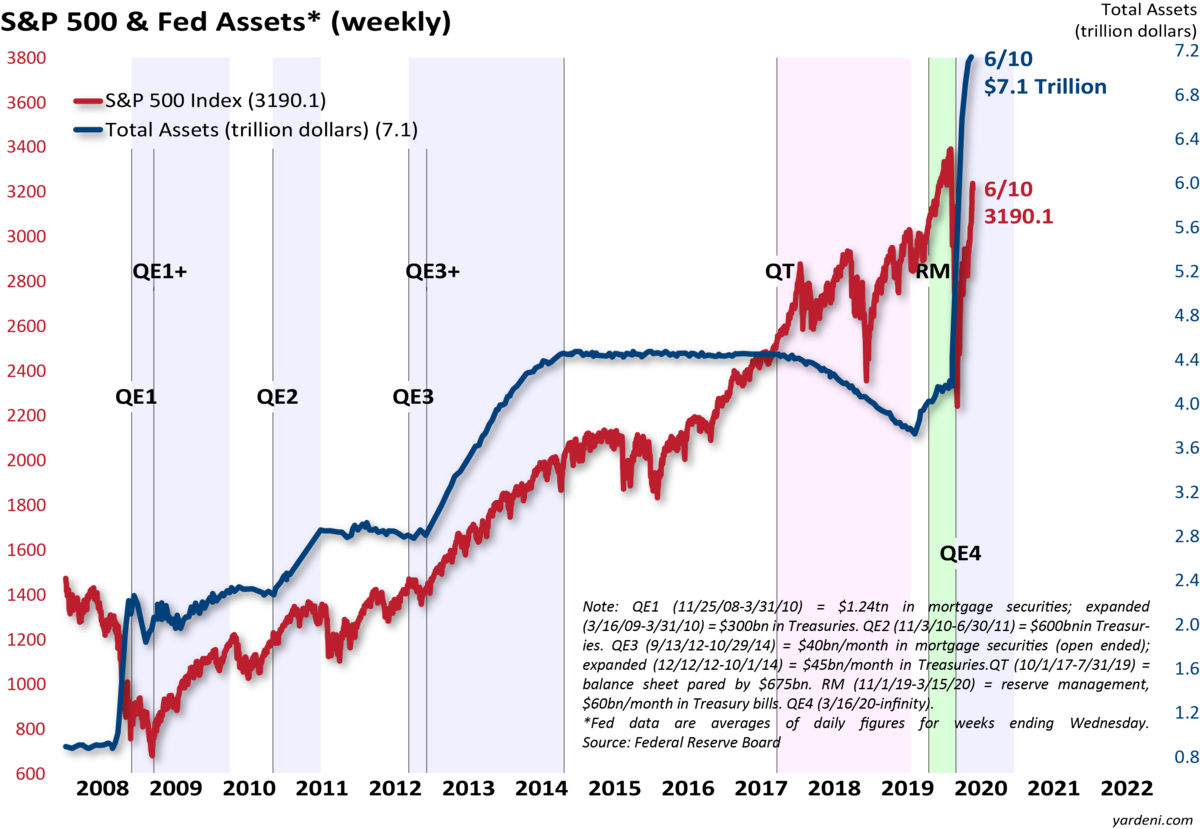

Figure 9. | S&P 500 & Fed Assets* (weekly)

The Fed’s easy monetary policy can be seen by the growth of its balance sheet since QE1 was launched in the midst of the Credit Crisis. Virtually all of the market’s gains since 2009 have come when the Fed has been expanding its balance sheet. The Fed response to the virus-induced recession turbocharged its balance sheet. Since February 26, the Fed’s balance sheet has swelled by $3 trillion to $7.1 trillion, up 73%. It’s not just the Fed; the combined balance sheets of the Fed, the ECB, the Bank of Japan, and the Bank of China are almost $25 trillion.

It seems like it is just the beginning for the Fed. Recently Fed Chairman Powell said “We’re not even thinking about raising rates. We are strongly committed to using our tools to do whatever we can for as long as it takes.”

In our January Market Outlook, we discussed the fact that the Fed has not been able to maintain their 2.0% inflation target for over 20 years. In our opinion a big part of that is the debt burden. More debt equates to slower economic growth, less inflation pressures, and lower interest rates.

Now that the Fed is printing money like a drunken sailor, the money supply aggregates are surging. Will the skyrocketing monetary base and money supply lead to price inflation? It doesn’t appear so yet. It is interesting to look at the velocity of money, which is how quickly money turns over in the economy. More velocity leads to more inflation, and vice versa. Right now, the velocity of money is hitting record lows, indicating that inflation is not a worry. When velocity turns up, we will likely see inflation start to rise.

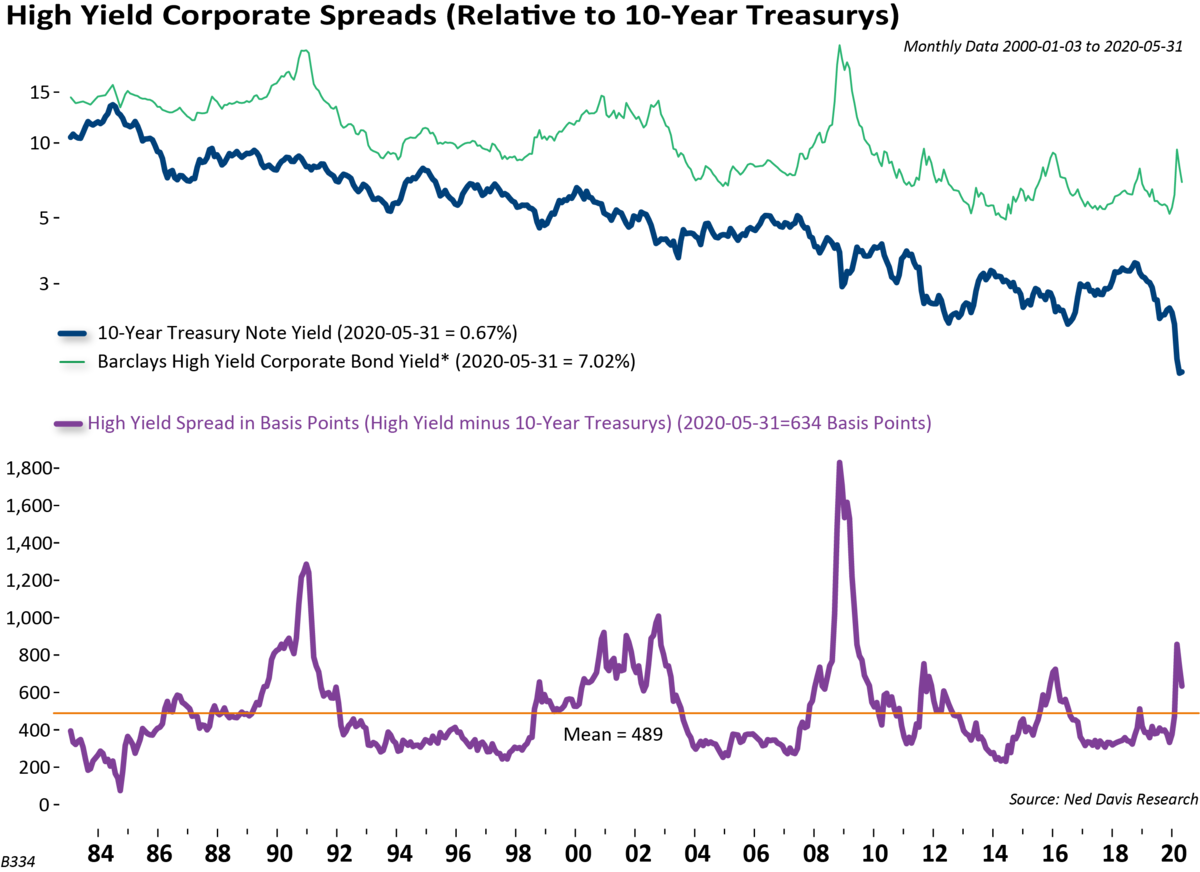

Figure 10. | High Yield Corporate Spreads (Relative to 10-Year Treasuries)

Credit spreads blew out during the March sell-off with high yield spreads reaching 1100 bps. We turned bullish on credit on March 27th, just four days off the low, buying high yield debt. Spreads have collapsed to 600 bps and look to come in even more. The Fed support that was announced on this past Monday, along with continued buying of corporate bonds by the ECB and BOJ, signals that corporate credit, both investment grade and high yield, may be positioned to continue moving higher.

The Fed’s announced updates to the Secondary Market Corporate Credit Facility and stated it “will begin buying a broad and diversified portfolio of corporate bonds to support market liquidity and the availability of credit for large employers.”

While the central banks have the short end under control, the long end of the curve is determined by supply, economic growth, and inflation expectations. In addition to massive amounts of sovereign issuance, there has been a record amount of corporate issuance.

A big risk, in our view, is how long the market absorbs the massive amount of debt issuance. Investment grade and high yield issuance is up 90% and 57%, year over year, respectively. Interest rates are low, so debt service is manageable, but it is causing a material deterioration in net leverage ratios. In both the investment grade and high yield markets, companies have responded to the crisis by increasing gross leverage, which has allowed them to strengthen their liquidity positions. Should the economic recovery disappoint, the recent increase in leverage could be a longer-term problem.

With all of the fiscal spending, we would remiss if we don’t talk about the rising budget deficit. The Federal Government will continue providing support to the economy. There have already been four relief packages totaling $2.4 trillion, and there will be more to come. The fiscal situation prior to the crisis was bad, we believe it will continue to worsen. Spending is up and tax revenues will plummet, further widening the deficit and adding to the national debt.

This will likely present long-term structural problems. No one on either side of the aisle had fiscal restraint prior to the crisis and now we seem to have full-on Modern Monetary Policy. If there is any silver lining here, it is that interest rates are so low that servicing all of this new debt is easier. This also supports the case for keeping rates lower for longer.

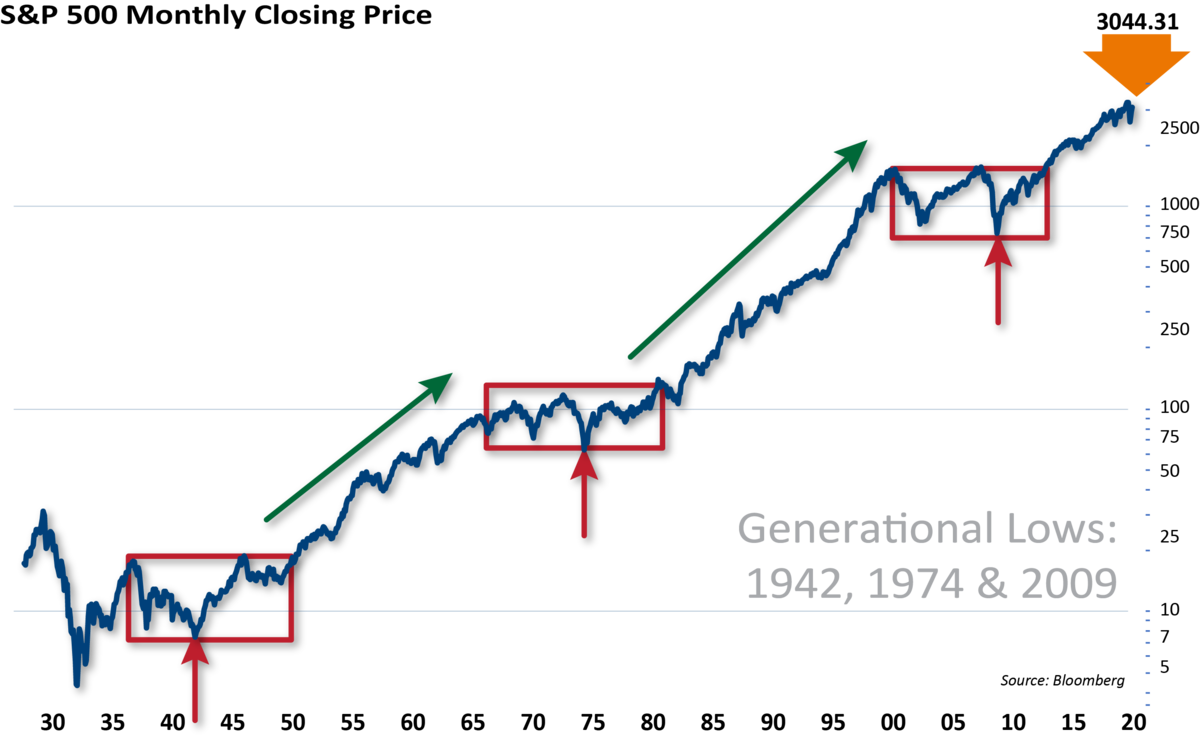

Figure 11. | S&P 500 Monthly Closing Price

The Way Forward: The Shortest Recession on Record?

We have concluded the past several annual Market Outlooks with the above chart of the very long-term perspective of the equity markets.

This chart of the S&P 500 dates back into the 1920s. The three boxes in red highlight the last three secular bear markets. Note that once the market eclipsed its prior secular peak, it continued higher for many years. The prior two secular bull runs lasted 22 and 18 years. We are still in the secular bull market that began after the Credit Crisis. If history is any guide, the probability of additional secular gains is high. However, we will be monitoring this very closely for any change in the secular winds given the current economic and social crisis, as well as the deteriorating fiscal position.

In conclusion, we have witnessed an epic economic collapse, market decline and recovery with a speed and intensity like never before. We will see the worst quarter of economic decline in history in the current quarter, but the economy looks to have already bottomed. We anticipate this will end up being the shortest recession on record. We also expect a strong economic recovery in the second half of the year and then to resume a slower growth trajectory into the future. For the markets, given the sharp recovery, it is imperative that earnings rebound sharply to ease the valuation concerns. The Fed has the market’s back, as long as they are flooding the system with liquidity, and we can expect the market to remain resilient. We are likely to see additional bouts of volatility this year, especially as the election heats up. Finally, the amount of debt being accumulated across sovereign, corporations, and municipalities presents a structural longer-term issue that one day will have to be dealt with.

Eager for More Insights? Visit our 2020 Mid-Year Market Outlook Resource Center.

The views expressed are those of the author(s) and do not necessarily reflect the views of Clark Capital Management Group. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Clark Capital investments portfolio. Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, other investments or to adopt any investment strategy or strategies. For educational use only. This information is not intended to serve as investment advice. This material is not intended to be relied upon as a forecast or research. Past performance does not guarantee future results.

The S&P 500 measures the performance of the 500 leading companies in leading industries of the U.S. economy, capturing 75% of U.S. equities.

The 10-year Treasury note is a debt obligation issued by the United States government with a maturity of 10 years upon initial issuance. A 10-year Treasury note pays interest at a fixed rate once every six months and pays the face value to the holder at maturity.

The Dow Jones Industrial Average is the most widely used indicator of the overall condition of the stock market, a price-weighted average of 30 actively traded blue chip stocks, primarily industrials. The 30 stocks are chosen by the editors of the Wall Street Journal (which is published by Dow Jones & Company), a practice that dates back to the beginning of the century. The Dow is computed using a price-weighted indexing system, rather than the more common market cap-weighted indexing system.

NDR (Ned Daily Research) Daily Trading Sentiment Index is based on the S&P 500 Daily Sentiment Index which shows a short-term sentiment view of the S&P 500 Index

Created by the Chicago Board Options Exchange (CBOE), the Volatility Index, or VIX, is a real-time market index that represents the market’s expectation of 30-day forward-looking volatility. Derived from the price inputs of the S&P 500 index options, it provides a measure of market risk and investors’ sentiments.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

This document may contain certain information that constitutes forward-looking statements which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology (or the negative thereof). Forward looking statements cannot be guaranteed. No assurance, representation, or warranty is made by any person that any of Clark Capital’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

The Composite Index of Leading Indicators, otherwise known as the Leading Economic Index (LEI), is an index published monthly by The Conference Board. It is used to predict the direction of global economic movements in future months. The index is composed of 10 economic components whose changes tend to precede changes in the overall economy. The Conference Board is an independent research association that provides its member organizations with economic and financial information.

The volatility (beta) of a client’s portfolio may be greater or less than its respective benchmark. It is not possible to invest in these indices.

Index returns include the reinvestment of income and dividends. The returns for these unmanaged indexes do not include any transaction costs, management fees or other costs. It is not possible to make an investment directly in any index.

Clark Capital Management Group, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Clark Capital’s advisory services and fees can be found in its Form ADV which is available upon request. CCM-672

![]()