Economy Slows Dramatically as Slowing the Virus Takes Priority

HIGHLIGHTS:

- The volatility that began in late February soared in March as the coronavirus outbreak grew in the United States. The VIX Index, a measure of volatility, closed at its highest point ever on March 16, which marked only the 3rd time in its history it had closed above 80.

- The longest running bull market on record ended in dramatic fashion in mid-March. The S&P 500 Index hit an all-time high on 2/19 and the 20% drop was the fastest from a peak level in history, occurring in just 16 trading days.

- Bonds also came under pressure in March. Driven in part by record outflows from bond mutual funds, bond prices fell, and spreads widened in municipal, investment grade and high-yield bonds as liquidity dried up.

- A flight to quality drove U.S. Treasury yields to historic lows. The 10-year U.S. Treasury yield closed at 0.54% on March 9 with the 30-year U.S. Treasury yield closing at 0.99% the same day. While volatile during the month, Treasury yields dropped sharply overall in March.

- The Fed acted quickly to try to provide ample liquidity to the financial markets. Following two emergency meetings, the FOMC cut rates to a range of 0% to 0.25%, announced an unlimited quantitative easing program, stepped in to support repo markets, and announced a facility to purchase commercial paper.

- In late March, the government announced a fiscal stimulus plan totaling about $2 trillion. The goal of this plan is to help bridge this period when economic activity will slow dramatically as non-essential businesses close and many Americans stay at home to slow the spread of COVID-19 and save lives.

EQUITY MARKETS

The volatility experienced in equity markets was in many ways unprecedented during March. The CBOE Volatility Index or VIX Index hit a record high during March. This index and its predecessor have been around since January 1990. Only three times in the over 7,600 trading days since its inception has this index closed above 80, including March 16, 2020 when it closed at 82.69 – a record high. Again, while we acknowledge that these are uncertain times, we do not believe that this is the scariest time in the last 30 years. The last time the VIX Index closed above 80 was November 20, 2008 right in the jaws of the financial crisis. Although past performance is not indicative of future results, the S&P 500 was up 20.1% six months after that date.

Volatility will likely remain elevated. According to Ned Davis Research, after the 18 previous cases in which the VIX has first broken above 30, a mean of 42 market days have passed before the VIX finally dropped below 30 and stayed below that level. The historical tendency is for volatility to remain elevated over the three-month period following spikes above 30.

Furthermore, the Dow Jones Industrial Average fell over 28% in a 5-day span, which has only been rivaled four other times in history. Those four times were the outbreak of World War I, the crash in 1929, the crash in 1987 and the five days following the Lehman Brothers bankruptcy in 2008. These were very uncertain times. Today, we feel there is a much clearer path to recovery than at those times as preventative measures like social distancing, limiting gatherings, cancelling sporting events and telecommuting take hold. It is easier for us to see the light at the end of the tunnel today than it was during those four world-changing events.

We had anticipated a more volatile ride moving into 2020 due in part to valuations getting stretched after the year-end run in 2019, optimism reaching extreme levels (which can be a bearish indicator of complacency in the market), and normal volatility that markets historically experience in the first half of a presidential election year. We had even believed that a 5%-10% correction could materialize in the first part of 2020.

Clearly, we did not anticipate COVID-19 and the impact it would have on our economy and financial system. As markets declined in March, however, valuations improved with stock prices going down. Admittedly, the earnings picture is a significant unknown as many companies are pulling their own guidance, and we expect a significant drop off in earnings in the months ahead. However, the stretched valuations we saw at the beginning of the year are no longer an issue in our opinion. There will be a material impact on the global economy due to the coronavirus and the impact on corporate earnings will be meaningful as well. At this point, trying to determine growth or earnings estimates is difficult.

Extremes have been reached on the pessimistic side when looking at indicators like the VIX Index, trading sentiment and put/call ratios. We tend to see these types of extreme pessimistic readings as the market is going through a bottoming process. Nobody can predict when the exact bottom gets put in place in the market, but pessimism has reached extremes and severe oversold conditions developed during March.

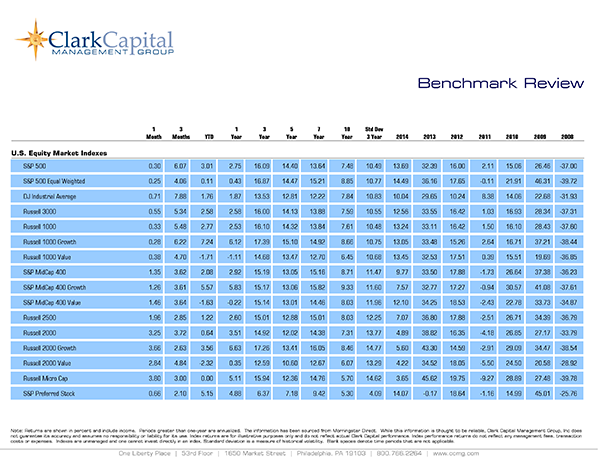

With this background, equities suffered through a difficult month and quarter. The numbers for March were as follows: The S&P 500 was down -12.35%, the Dow Jones Industrial Average was off -13.62%, the Russell 3000 declined -13.75%, the NASDAQ Composite slid by -10.03% and the Russell 2000 Index, a measure of small-cap companies, was among the hardest hit as it fell -21.73%. Quarterly declines (in the same order) were: -19.6%, -22.73%, -20.9%, -13.95%, and -30.61%, respectively. Growth stocks continued to outpace value stocks on a relative basis rather dramatically for the month and quarter. The large-cap and value focused Russell 1000 Value Index declined -17.09% compared to the Russell 1000 Growth Index, which fell by -9.84% in March. Large-cap stocks also held a clear relative advantage to small and mid-cap stocks for the month and quarter.

International equities struggled as well in March and the first quarter. Emerging market equities, as measured by the MSCI Emerging Markets Index, fell -15.4% in March and declined -23.6% for the quarter. The MSCI ACWI ex USA Index, a broad measure of international equities, fell -14.48% for the month and -23.36% for the quarter. The U.S. dollar was also very volatile in March. After sliding to a more than one-year low early in the month, it rebounded sharply to its highest level since late 2016 before settling only modestly above where it closed February.

FIXED INCOME

It wasn’t only stocks that came under pressure in March as bond markets fell when liquidity dried up. The Fed stepped in aggressively and enacted several measures to try to improve liquidity and ease some of the stress in the bond markets. One source of stress was the record level of bond mutual fund outflows experienced during different weeks in March. According to Lipper, investors pulled $62 billion from taxable bond funds and $13 billion from municipal bond funds during the week of March 25th – both were weekly outflow records, eclipsing records set the prior week.

The flight-to-quality trade was the clear winner in March as U.S. Treasury yields hit historic lows and Treasury prices rallied. However, other pockets of fixed income declined during the month as bonds that trade with a spread to Treasury yields saw that spread widen during the month meaning those bond prices went down.

It is important to keep in mind that a sell-off in the fixed income markets or a rise in rates may temporarily lower the account value for the individual bond holder. However, if held to maturity, and if the issuer does not default, individual bond holders will receive two interest payments per year and par value when the bonds mature and will earn a positive return.

The yield on the 10-year U.S. Treasury closed March 9th at 0.54%, a historic low. The yield closed out March at 0.7% compared to the February close of 1.13% and the 2019 close at 1.92%. Driven by a declining interest rate environment, but also one where spreads widened, the returns for the month of March in fixed income were as follows: the Bloomberg Barclays U.S. Aggregate Bond Index fell -0.59%, the Bloomberg Barclays U.S. Credit Index declined -6.63%, and the Bloomberg Barclays U.S. Corporate High Yield Index dropped by -11.46%.

For the quarter, those index results were as follows: a gain of 3.15%, and declines of -3.14% and -12.68%, respectively. Municipal bonds declined for the month and quarter as well. The Bloomberg Barclays U.S. 30 Year Treasury index advanced 7.56% in March and 25.80% for the quarter, while the general Bloomberg Barclays U.S. Treasury index gained 2.89% and 8.2% for the month and quarter, respectively.

ECONOMIC DATA AND OUTLOOK

Economic data released in March that largely covered February activity, remained for the most part solid. This period missed most of the mounting impact of the coronavirus epidemic as many companies started to slow operations and people started staying at home during the month of March.

We anticipate that economic data in the weeks and months ahead will be bad and we believe the second quarter will bear the brunt of the economic damage. GDP is going to be down significantly in the second quarter and jobless claims and the unemployment rate will skyrocket.

With many consumers confined to their homes, we anticipate retail spending will fall dramatically as well. We believe the third quarter will be a period of transition as people start going back to work and the re-opening process for many businesses begins. The fourth quarter should be a rebound quarter and is likely to exhibit stronger than trend growth as depleted inventories are replenished and pent up demand from consumers is unleased. We anticipate that 2021 will be a rebound year economically.

Just to put some numbers on this and with the full understanding that trying to come up with estimates is difficult under current conditions, we believe that first quarter GDP will be marginally positive, at best, with a 1% growth rate. We expect second quarter GDP to decline somewhere between 10%-15%. The third quarter will likely be a transition period and may have a negative or slightly positive economic growth rate, which largely depends on how quickly active cases peak in the U.S. and when social behavior returns to some normalcy. We believe the fourth quarter should be a rebound quarter that will likely exhibit stronger than trend growth and we expect at least 5% GDP growth.

The Federal Reserve (Fed) has been front and center trying to combat this crisis from the monetary policy side. The Fed has cut rates to a range of 0% to 0.25% (the same level rates were at during the credit crisis in December 2008) and embarked on another quantitative easing program buying unlimited amounts of U.S. Treasury securities and agency mortgage-backed securities.

Other actions by the central bank include pumping massive amounts of liquidity into the financial system through repurchase agreements or the repo market, and suspending reserve requirements for banks and putting in place a facility to by commercial paper – a key funding source that large companies use to finance their short-term cash needs. The Fed took these measures to help keep the financial system functioning properly as they do not want this health crisis to turn into a financial crisis.

The fiscal stimulus that will amount to about $2 trillion was signed into law in late March. Some components of this package include sending money directly to U.S. citizens based on income levels, boosting and extending unemployment insurance, creating a $500 billion pool for loans to companies, states and municipalities, and supporting industries directly impacted by this crisis, like airlines. This is not an exhaustive list, but the main goal of this package is to bridge the period when the economy slows down significantly until the country starts to re-open businesses more broadly. There is even some initial talk that another stimulus package focused on infrastructure spending might be considered next.

Although it is hard to put a precise number on it, efforts by the Fed plus the fiscal stimulus plan appear to total near $6 trillion in an effort to bolster the economy. The United States is about a $20 trillion economy, so that is a lot of money when you put it into perspective. It will take some time for the stimulus to works its way into the economy and inevitably the naysayers will argue the stimulus is not working. However, we believe that the stimulus will ultimately work and will have a positive impact on the economy.

We understand that the market is focused on many variables these days and prior economic releases are likely not of central importance at this time. However, we do think it is important to cover a few of the economic highlights from last month just as a reminder of the solid footing the economy was on before we were hit by this exogenous event.

The Institute for Supply Manufacturing (ISM) Non-Manufacturing Index was above expectations for February and although the ISM Manufacturing Index fell short of estimates, it remained just above 50, which is the dividing line between expansion and contraction. Payroll additions were well above expectations and the unemployment rate at 3.5% was better (lower) than expected in February and continued to hover near its lowest level in about 50 years.

Retail sales (ex. autos and gas) fell in February when a gain was expected, but the prior month’s reading was revised higher to show stronger growth than previously reported for January. Housing starts, existing, and new home sales all surpassed estimates, but building permits fell short of expectations.

INVESTMENT IMPLICATIONS

Clark Capital’s Top-Down, Quantitative Strategies

The S&P 500 experienced its fastest ever slide into bear market territory from new all-time highs. The S&P 500 fell almost 34% from peak to bottom, before rallying into month end. In the midst of the decline, volatility spiked with the CBOE Volatility Index hitting it highest level ever.

We believe our top-down, quantitatively driven portfolios were well positioned for this decline with a defensive bias. The Style Opportunity portfolio is overweight large-cap and growth. In addition, Navigator® Fixed Income Total Return (FITR) de-risked on 2/26 and 3/9, moving into U.S. Treasuries. However, after recent stabilization in credit markets, the models that guide the FITR strategy turned positive on high yield debt and as a result, the strategy is now allocated 100% back into high yield bonds.

Clark Capital’s Bottom-Up, Fundamental Strategies

The threat to global growth and lower interest rates have pushed the equity portfolios away from Financials, Industrials, Energy and Materials and we remain underweight these sectors. Energy, Materials, and travel related sectors have been hit the hardest in through this crisis.

Technology and Healthcare remain our largest equity overweights, with both sectors having fared better given the increased focus on technology efficiencies while we “shelter-in-place” and the need for more healthcare related services in the crisis.

We know these are difficult and challenging times. We also know that we will see bad news in the short-term, which is causing some of the extreme volatility we are seeing in the capital markets today. However, stocks are forward looking, and the market will bottom before the bad news stops being reported. We believe that the U.S. economy and corporate America will come through this crisis, although it might take some time. We would not bet against the resiliency of the U.S. economy, corporate America and U.S. citizens to fight their way through this challenging period.

We believe it is imperative for investors to stay focused on their long-term goals and not let these short-term swings in the market derail them from their longer-term objectives.

| Event | Period | Estimate | Actual | Prior | Revised |

|---|---|---|---|---|---|

| ISM Manufacturing | Feb | 50.5 | 50.1 | 50.9 | — |

| ISM Non-Manf. Composite | Feb | 54.8 | 57.3 | 55.5 | — |

| Change in Nonfarm Payrolls | Feb | 175k | 273k | 225k | 273k |

| Unemployment Rate | Feb | 3.60% | 3.50% | 3.60% | — |

| Average Hourly Earnings YoY | Feb | 3.00% | 3.00% | 3.10% | — |

| JOLTS Job Openings | Jan | 6400k | 6963k | 6423k | 6552k |

| PPI Final Demand MoM | Feb | -0.10% | -0.60% | 0.50% | — |

| PPI Final Demand YoY | Feb | 1.80% | 1.30% | 2.10% | — |

| PPI Ex Food and Energy MoM | Feb | 0.10% | -0.30% | 0.50% | — |

| PPI Ex Food and Energy YoY | Feb | 1.70% | 1.40% | 1.70% | — |

| CPI MoM | Feb | 0.00% | 0.10% | 0.10% | — |

| CPI YoY | Feb | 2.20% | 2.30% | 2.50% | — |

| CPI Ex Food and Energy MoM | Feb | 0.20% | 0.20% | 0.20% | — |

| CPI Ex Food and Energy YoY | Feb | 2.30% | 2.40% | 2.30% | — |

| Retail Sales Ex Auto and Gas | Feb | 0.30% | -0.20% | 0.40% | 0.70% |

| Industrial Production MoM | Feb | 0.40% | 0.60% | -0.30% | -0.50% |

| Building Permits | Feb | 1500k | 1464k | 1551k | 1550k |

| Housing Starts | Feb | 1500k | 1599k | 1567k | 1624k |

| New Home Sales | Feb | 750k | 765k | 764k | 800k |

| Existing Home Sales | Feb | 5.51m | 5.77m | 5.46m | 5.42m |

| Leading Index | Feb | 0.10% | 0.10% | 0.80% | 0.70% |

| Durable Goods Orders | Feb P | -0.90% | 1.20% | -0.20% | 0.10% |

| GDP Annualized QoQ | 4Q T | 2.10% | 2.10% | 2.10% | — |

| U. of Mich. Sentiment | Mar F | 90 | 89.1 | 95.9 | — |

| Personal Income | Feb | 0.40% | 0.60% | 0.60% | — |

| Personal Spending | Feb | 0.20% | 0.20% | 0.20% | — |

| S&P CoreLogic CS 20-City YoY NSA | Jan | 3.20% | 3.08% | 2.85% | 2.84% |

Source: Bloomberg

Past performance is not indicative of future results. The opinions expressed are those of the Clark Capital Management Group portfolio manager(s) that manage the strategies or products discussed herein, and do not necessarily reflect the opinions of all portfolio managers at Clark Capital Management Group or the firm as a whole. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, other investments or to adopt any investment strategy or strategies.

There is no guarantee of the future performance of any Clark Capital investment portfolio. This is not financial advice or an offer to sell any product. Clark Capital Management Group reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. It should not be assumed that any of the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. Clark Capital Management Group is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Clark Capital Management Group’s advisory services can be found in its Form ADV which is available upon request.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed. Nothing herein should be construed as a solicitation to buy, sell or hold any securities, other investments or to adopt any particular investment strategy or strategies. For educational use only.

The Dow Jones Industrial Average indicates the value of 30 large, publicly owned companies based in the United States.

The NASDAQ Composite is a stock market index of the common stocks and similar securities listed on the NASDAQ stock market.

The S&P 500 measures the performance of the 500 leading companies in leading industries of the U.S. economy, capturing 75% of U.S. equities. .

The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 Index companies with lower price-to-book ratios and lower forecasted growth values.

The Russell 2000 Index is a small-cap stock market index that represents the bottom 2,000 stocks in the Russell 3000.

The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

The 10 Year Treasury Rate is the yield received for investing in a US government issued treasury security that has a maturity of 10 year. The 10 year treasury yield is included on the longer end of the yield curve. Many analysts will use the 10 year yield as the “risk free” rate when valuing the markets or an individual security.

The 30 Year Treasury Rate is the yield received for investing in a US government issued treasury security that has a maturity of 30 years. The 30 year treasury yield is included on the longer end of the yield curve and is important when looking at the overall US economy

The MSCI Emerging Markets Index is used to measure large and mid-cap equity market performance in the global emerging markets.

The MSCI ACWI ex USA Index captures large and mid-cap representation across 22 of 23 developed market countries and 24 emerging market countries, covering approximately 85% of the global equity opportunity set outside of the U.S.

Bloomberg Barclays U.S. Aggregate Bond Index: The index is unmanaged and measures the performance of the investment grade, U.S. dollar denominated, fixed-rate taxable bond market, including Treasuries and government-related and corporate securities that have a remaining maturity of at least one year.

The Bloomberg Barclays U.S. Corporate High-Yield Index covers the U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below.

The Bloomberg Barclays U.S. Credit Index measures the investment grade, U.S. dollar denominated, fixed-rate taxable corporate and government related bond markets.

The Bloomberg Barclays 30-Year U.S. Treasury Index is a universe of Treasurybonds, and used as a benchmark against the market for long-term maturityfixed-income securities. The index assumes reinvestment of all distributionsand interest payments.

The ISM Non-Manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms’ purchasing and supply executives, within 60 sectors across the nation, by the Institute of Supply Management (ISM). The ISM Non-Manufacturing Index tracks economic data, like the ISM Non-Manufacturing Business Activity Index. A composite diffusion index is created based on the data from these surveys, that monitors economic conditions of the nation.

Personal consumption expenditures price index is the component statistic for consumption in gross domestic product collected by the United States Bureau of Economic Analysis.

The CBOE Volatility Index, known by its ticker symbol VIX, is a popular measure of the stock market’s expectation of volatility implied by S&P 500 index options.

The volatility (beta) of a client’s portfolio may be greater or less than its respective benchmark. It is not possible to invest in these indices.

Index returns include the reinvestment of income and dividends. The returns for these unmanaged indexes do not include any transaction costs, management fees or other costs. It is not possible to make an investment directly in any index.

CCM-993

![]()