Stocks Recover and Bonds Rebound Sharply in November

HIGHLIGHTS:

- The 3-month losing streak for stocks ended with a solid recovery during November. More dramatically, bonds rebounded strongly during the month as yields dropped sharply from multi-year highs hit in October.

- After closing October at just over 18, the VIX Index (a measure of stock market volatility) dropped in November and closed the month at just below 13 as stocks rallied and fear levels subsided.

- As yields fell, bond prices also rallied in November. The yield on the 10-year U.S. Treasury hit 5% intraday for the first time since 2007 in October and closed that month at 4.88%. November saw the yield drop below 4.3% at times and it closed the month at 4.37%. This drop in rates and subsequent rally in bond prices was a welcome relief for bond investors.

- The FOMC concluded a meeting on November 1 and as expected, it left policy rates unchanged. As markets gained confidence that this rate-tightening cycle might be over, stocks rallied, and yields fell in November.

- The U.S. economy continues to grow, but Q4 growth will likely pale in comparison to the torrid pace of growth from Q3. However, more modest growth might give the Fed cover to hold off on additional rate hikes as inflation pressures lessen as well.

- Finally, corporate earnings are improving and expected to grow in calendar years 2023 and 2024. While expected earnings growth has moderated somewhat for 2023, earning expectations for 2024 have remained solid.

EQUITY MARKETS

The 3-month streak of stock declines was broken in November. Negative sentiment appeared to get overdone after the 10% correction seen from the beginning of August through late October, as fundamentals remained solid. Stocks rallied throughout the month of November as we entered what is seasonally the strongest three months of the year. With the market gaining confidence that this Fed rate hike cycle might be over, stocks rebounded, and rates dropped dramatically leading to a solid month of gains in both stocks and bonds. See Table 1 for equity results for November and year to date.

Table 1

| Index | November 2023 | YTD |

|---|---|---|

| S&P 500 | 9.13% | 20.80% |

| S&P 500 Equal Weight | 9.14% | 6.56% |

| DJIA | 9.15% | 10.72% |

| Russell 3000 | 9.32% | 19.61% |

| NASDAQ Comp. | 10.83% | 37.00% |

| Russell 2000 | 9.05% | 4.20% |

| MSCI ACWI ex U.S. | 9.00% | 10.09% |

| MSCI Emerging Mkts Net | 8.00% | 5.70% |

As has been the case for most of the year, large-cap growth led this rally, but gains were widespread in November. Gains in November were able to push the S&P 500 Equal Weight Index, the Russell 2000 Index, and the MSCI Emerging Markets Index back into positive territory on a year-to-date basis.

Comparing and contrasting the S&P 500 Index with its equal-weighted counterpart provides important insight into this market. Driven by the strong performance of mega cap technology companies, the S&P 500 Index shows a solid year-to-date gain of 20.8%. However, the equal-weight S&P 500 Index (which can be thought of as representing what the average stock is doing) is showing more modest gains of 6.56%. Simply said, the largest cap Technology companies, which have a larger weighting in the S&P 500 Index, have been the primary drivers of this narrow market in 2023.

Meanwhile, the average stock return has been more muted so far this year with small-caps showing the weakest relative results. However, the good news is the rally broadened in November with gains across styles, market caps and geographies. The large-cap focused Russell 1000 Index gained 9.34% in November, with the growth version of this index up 10.90%, and the value version advancing 7.54%. For the year, the Russell 1000 Growth Index is up 36.63%, while the value version has gained a mere 5.61%. Large-cap growth has dominated this year, while value and small caps have been much weaker on a relative basis.

Broad international equities showed solid returns in November as well. The MSCI ACWI ex. U.S. Index was up 9.00% in November and the MSCI Emerging Market Index rallied 8.00%. November gains account for almost all the year-to-date returns for the MSCI ACWI ex. U.S. Index and gains were strong enough to push emerging markets back into positive territory year to date. We still see opportunities in international markets with valuations that are lower than the U.S. and our expectation that the U.S. dollar will largely weaken over the short-to-intermediate term.

While not necessarily a trend yet, coinciding with the market gaining confidence around the conclusion of this rate-hike cycle, the dollar weakened in November.

Fixed Income

The rally in bonds was dramatic in November. The grind higher in rates over the last several months had dragged bond returns down with most major bond indices ending in negative territory year-to-date through October. However, November saw bond yields drop sharply, and bonds staged a significant rally during the month. It is a good reminder that yields can move quickly at times and it is important for bond investors to stay focused on their long-term goals during periods of volatility.

We know the vast majority of a bond’s return is interest income and the reinvestment of that income, but when rates are moving, bond prices can fluctuate in the short term. The 10-year U.S. Treasury yield, which had been trending higher in recent months, dropped in November from 4.88% (October’s close) to 4.37% by the end of November. That decline in rates became a tailwind for bond returns and helped push most major bond indices back into positive territory year to date. See Table 2 for fixed income index returns for November and year to date.

Table 2

| Index | November 2023 | YTD |

|---|---|---|

| Bloomberg U.S. Agg | 4.53% | 1.64% |

| Bloomberg U.S. Credit | 5.68% | 3.83% |

| Bloomberg U.S. High Yld | 4.53% | 9.37% |

| Bloomberg Muni | 6.35% | 3.98% |

| Bloomberg 30-year U.S. TSY | 9.72% | -6.23% |

| Bloomberg U.S. TSY | 3.47% | 0.67% |

The move higher in rates overall in 2023 presents bond investors with what we believe are opportunities to invest at higher yields and coupons than seen in several years even with this move lower in rates in November. We expect the 10-year U.S. Treasury yield to move lower as we move into 2024, but we also anticipate volatility along the way. This month, volatility worked to investors’ advantage. The more interest rate sensitive pockets of the bond market (like U.S. Treasuries) have been the hardest hit by rising rates in 2023. The sharp decline in rates put the 30-year U.S. Treasury return into the top spot for the month, but the overall rise in rates in 2023 kept that index in last place year to date on Table 2.

We maintain our long-standing position favoring credit versus pure rate exposure in this interest rate environment. We also believe the role bonds play in a portfolio, to provide stable cash flow and to help offset the volatility of stocks in the long run, has not changed. Furthermore, we believe that bond yields are attractive in what are some of the highest yields we have seen in the last 15 years.

Economic Data and Outlook

Although rearview looking, Q3 2023 economic growth is worth a quick review. The second release of Q3 U.S. GDP was another surprise with annualized growth at 5.2% – the best rate of growth since the fourth quarter of 2021. This was revised higher from the initial estimate of 4.9% and surpassed expectations of 5.0%.

As expected, growth has appeared to moderate in the early part of the fourth quarter, but the economy is on solid footing and has been stronger than most expected so far in 2023. That said, we do expect growth to moderate as we close out 2023 and move into 2024 and we believe the rate hikes are still working their way through the economy and will likely result in a period of slower economic growth in 2024.

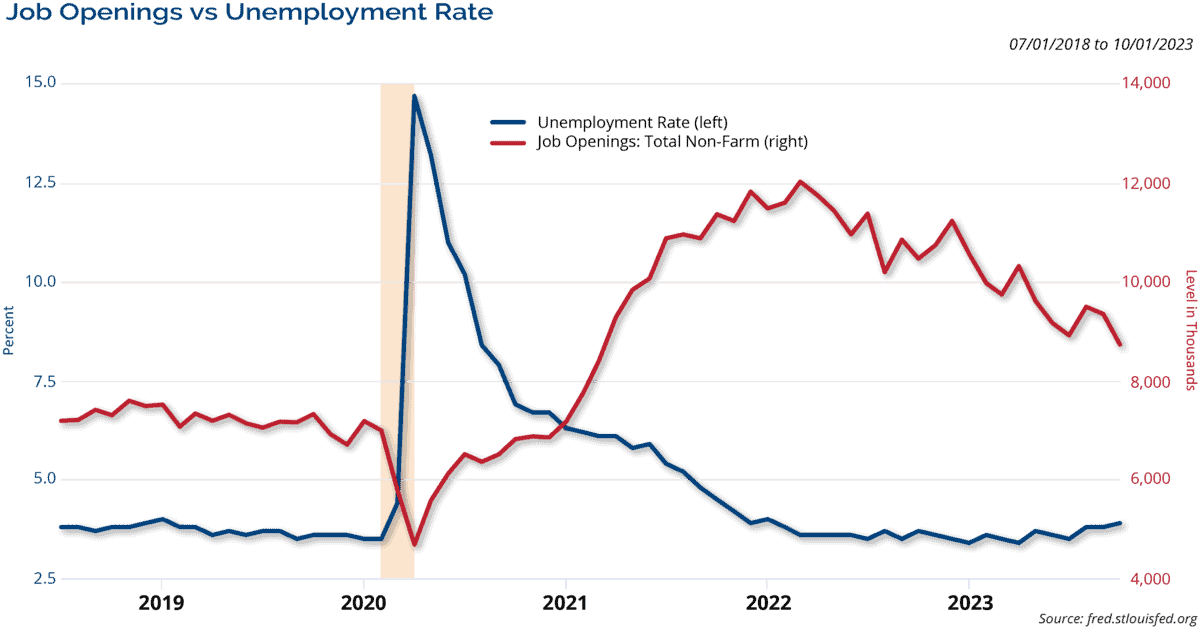

Job market progress continued in October, but the pace of gains slowed. Non-farm payroll additions were 150,000 in October, which was less than the 180,000 expected and barely half of the job gains from last month of 297,000. The unemployment rate ticked higher to 3.9% when it was expected to stay at the prior month’s level of 3.8%. While still low, it is noteworthy that this is the highest unemployment rate since January 2022 – the last time this rate was 4% or higher.

Average hourly earnings fell to a 4.1% annual increase from the prior reading of 4.3%, but it was still ahead of estimates of 4.0%. Job openings increased again in September to 9.553 million, easily surpassing expectations of 9.4 million. Job openings remain plentiful, but they are down from their peak levels. The aggressive rate hikes by the Fed might be having an impact on hiring decisions as job openings have trended lower and unemployment has ticked higher. However, the labor market remains solid with millions more jobs available compared to unemployed people. Chart 1 shows this relationship between job openings and the unemployment rate.

Chart 1

For illustrative purposes only.

For illustrative purposes only.

With the current strength in the job market, we maintain our opinion that it seems unlikely that the economy would slow too drastically under these conditions. However, even a modest slowdown in the job market could be a headwind to economic activity due to the central role that consumer spending plays in the U.S. economy. The odds of a soft landing have likely increased in recent months, particularly with the recent GDP report, but a reasonable probability of a mild recession still exists and should not be dismissed. We believe opportunities exist in the stock and bond markets under either of these two scenarios as consumers remain strong and the job market remains healthy.

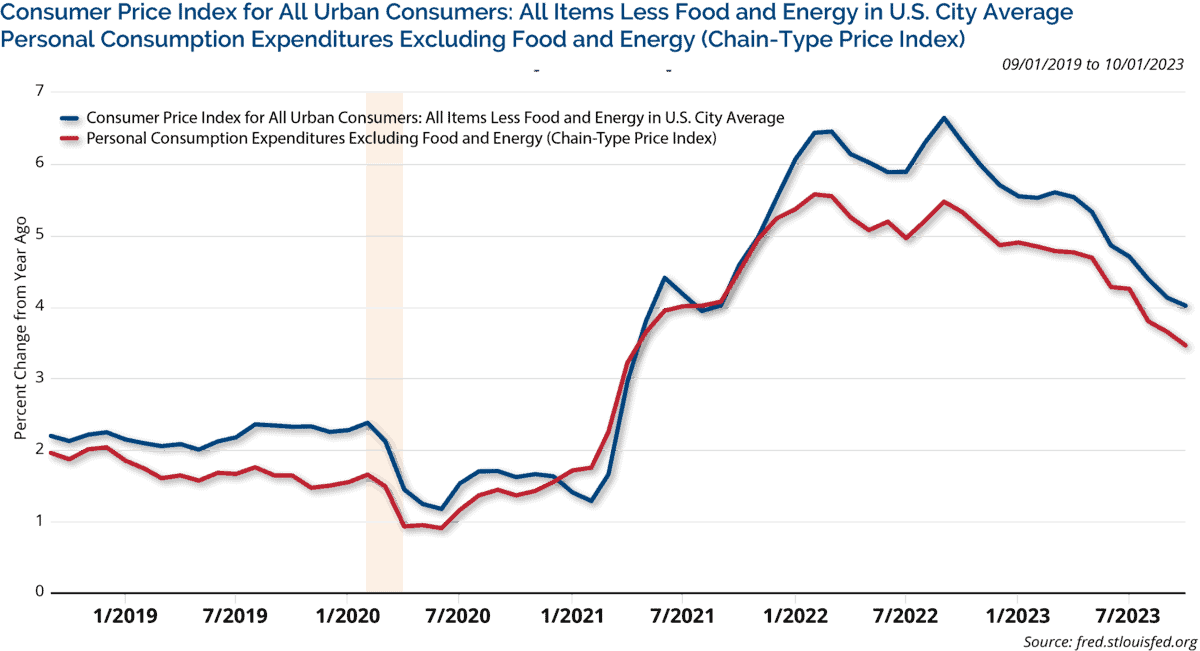

Positive inflation data seemed to be one of the primary catalysts that pushed stocks and bonds higher in November. The headline Consumer Price Index showed an annual increase of 3.2% in October, which beat expectations of 3.3% and was a drop from the prior month’s reading of 3.7%. The core CPI increased by 4.0% in October on an annual basis, which was flat from last month but better than estimates of 4.1%. The headline Producer Price Index showed a surprise monthly drop of -0.5% in October when an increase of 0.1% was anticipated. This made the annual gain 1.3%, which was better than the expected 1.9% increase and the prior month’s rise of 2.2%. The core PPI had an annual increase of 2.4% in October, which was better than expectations and the prior month’s mark of 2.7%. These improvements on the inflation front seemed to bolster the market’s belief that the Fed might be done with this rate hike cycle. After over a year and a half of “fighting the Fed”, the market reacted positively to data that supported the idea that this fight might be over.

Focusing on the preferred inflation measure of the Federal Reserve, the Personal Consumption Expenditures (PCE) Index showed a 3.0% annual gain in October, which was better than expectations of 3.1% and the prior month’s level of 3.4%. The core PCE reading (the reading the Fed targets) was 3.5%, in-line with expectations but an improvement from the September annual gain of 3.7%. The Fed’s preferred measure of inflation, the core PCE Price Index has improved, but it remains elevated from the Fed’s long-term target of around 2%. Chart 2 shows core consumer inflation readings – the core CPI Price Index and the core PCE Price Index.

Chart 2

For illustrative purposes only. For illustrative purposes only. Past performance is not indicative of future results.

For illustrative purposes only. For illustrative purposes only. Past performance is not indicative of future results.Clearly, progress has been made on inflation, but Fed Chairman Powell continues to reiterate that the inflation battle is not over. However, enough progress seems to have been made to keep the Fed on hold for the time being. The market is pricing in no more rate hikes, and it has clearly reacted positively to a Fed that appears to be on hold.

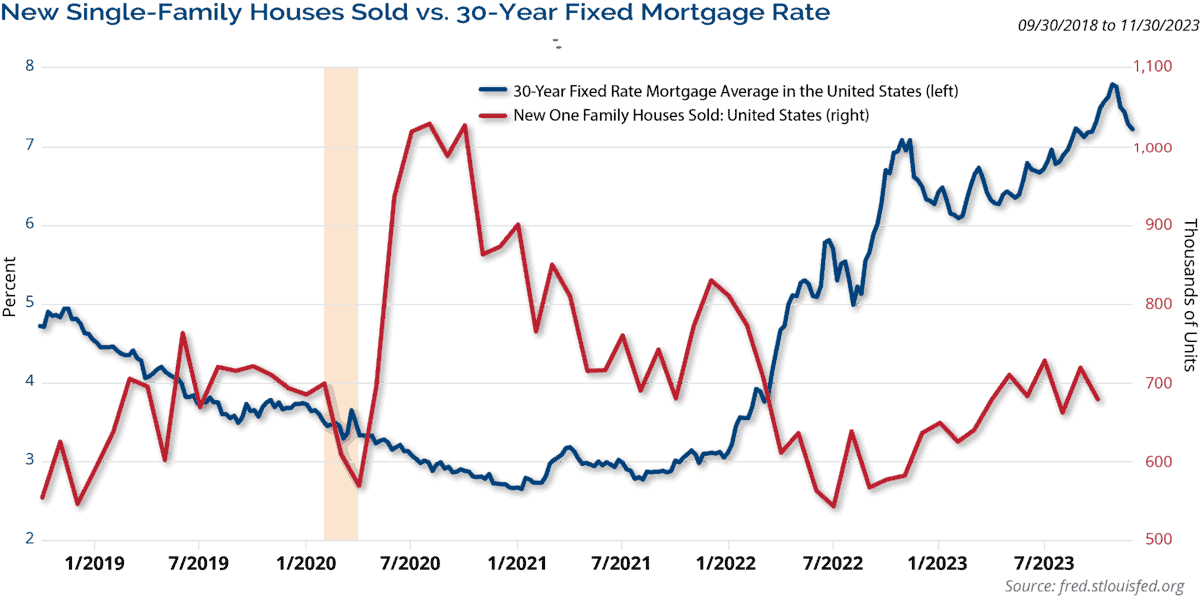

Mortgage rates surged toward 8% in October, which led to some mixed housing results. In October, building permits, considered a leading indicator for housing, were at an annualized pace of 1.487 million – above expectations of 1.450 million, and an increase from September’s level of 1.471 million. Housing starts surpassed expectations (1.350 million estimate versus 1.372 million reported), and this too was an improvement from the 1.346 million pace from September.

Existing home sales, however, slipped further below the 4 million annual rate level in October to 3.79 million – missing estimates of 3.90 million and dropping below the prior month’s 3.95 million annual pace. New home sales declined as well to a 679,000 annual rate. This level was below expectations of 721,000 and the prior month reading at a 719,000 annual pace. Home prices rose in September by 3.92%, which was more-or-less in line with expectations of a 3.90% increase based on the S&P CoreLogic 20-City Index. As previously mentioned, mortgage rates took another leg higher in October and stood at multi-year highs. Interest rates and mortgage rates did drop rather sharply in November, so it will be important to see how housing reacts in the months ahead. Chart 3 shows the relationship between mortgage rates and new home sales.

Chart 3

For illustrative purposes only. For illustrative purposes only. Past performance is not indicative of future results.

For illustrative purposes only. For illustrative purposes only. Past performance is not indicative of future results.The ISM Manufacturing Index for October was disappointing and marked the 12th straight month of contraction for this index. At 46.7, the index was lower than expectations and September’s mark of 49.0. (This index disappointed and stayed at 46.7 in November marking the 13th straight month of contraction.) The ISM Non-Manufacturing Index, which covers the much larger service industries in the U.S. economy, came in at 51.8 in October, a drop from the 53.6 reading the prior month, and disappointing compared to estimates of 53.0. Although the pace slowed, the service industries still reflected growth in October. Recall, the dividing line between expansion and contraction for the ISM indices is 50.

The health of U.S. consumers is being highly scrutinized due to their significant role in the U.S. economy. Retail sales (ex. auto and gas) rose by 0.1% in October, when a 0.2% gain was expected. However, the prior month’s surprisingly strong reading of a 0.6% increase was revised higher to a 0.8% gain.

The preliminary University of Michigan Sentiment reading for November dropped to 60.4 compared to expectations of 63.7 and the previous 63.8 level, which is not too surprising considering the weakness seen in the stock market over the last few months. (This reading is taken in the first half of the month just as the market was gaining some momentum.) The Conference Board’s Leading Index continued to decline and fell by -0.8% in October, which was worse than expectations of a -0.7% drop. For well over a year, the leading economic index has been flashing a warning sign of pending economic weakness which has yet to materialize to any large degree.

As always, we believe it is imperative for investors to stay focused on their long-term goals and not let short-term swings in the market derail them from their longer-term objectives.

Investment Implications

Clark Capital’s Top-Down, Quantitative Strategies

We have been fully risk-on across the tactical strategies including Fixed Income Total Return, Tactical Investment Grade, Global Tactical, and Global Risk Management since early November. We believe the markets and economy have a lot of momentum as we head into the end of the year.

Clark Capital’s Bottom-Up, Fundamental Strategies

After three months of negative returns, a resilient U.S. economy, lower rates and moderating inflation contributed to the outsized rally in November. In our bottom-up portfolios, dividend stocks have lagged the broader market year to date. Historically, the best period for dividend stocks is the 6 to 12 months following a final rate hike, which tends to be a late cycle period.

ECONOMIC DATA

| Event | Period | Estimate | Actual | Prior | Revised |

|---|---|---|---|---|---|

| ISM Manufacturing | Oct | 49.0 | 46.7 | 49 | — |

| ISM Services Index | Oct | 53.0 | 51.8 | 53.6 | — |

| Change in Nonfarm Payrolls | Oct | 180k | 150k | 336k | 297k |

| Unemployment Rate | Oct | 3.80% | 3.90% | 3.80% | — |

| Average Hourly Earnings YoY | Oct | 4.00% | 4.10% | 4.20% | 4.30% |

| JOLTS Job Openings | Sept | 9400k | 9553k | 9610k | 9497k |

| PPI Final Demand MoM | Oct | 0.10% | -0.50% | 0.50% | 0.40% |

| PPI Final Demand YoY | Oct | 1.90% | 1.30% | 2.20% | — |

| PPI Ex Food and Energy MoM | Oct | 0.30% | 0.00% | 0.30% | 0.20% |

| PPI Ex Food and Energy YoY | Oct | 2.70% | 2.40% | 2.70% | — |

| CPI MoM | Oct | 0.10% | 0.00% | 0.40% | — |

| CPI YoY | Oct | 3.30% | 3.20% | 3.70% | — |

| CPI Ex Food and Energy MoM | Oct | 0.30% | 0.20% | 0.30% | — |

| CPI Ex Food and Energy YoY | Oct | 4.10% | 4.00% | 4.10% | — |

| Retail Sales Ex Auto and Gas | Oct | 0.20% | 0.10% | 0.60% | 0.80% |

| Industrial Production MoM | Oct | -0.40% | -0.60% | 0.30% | 0.10% |

| Building Permits | Oct | 1450k | 1487k | 1473k | 1471k |

| Housing Starts | Oct | 1350k | 1372k | 1358k | 1346k |

| New Home Sales | Oct | 721k | 679k | 759k | 719k |

| Existing Home Sales | Oct | 3.90m | 3.79m | 3.96m | 3.95m |

| Leading Index | Oct | -0.70% | -0.80% | -0.70% | — |

| Durable Goods Orders | Oct P | -3.20% | -5.40% | 4.60% | 4.00% |

| GDP Annualized QoQ | 3Q S | 5.00% | 5.20% | 4.90% | — |

| U. of Mich. Sentiment | Nov P | 63.7 | 60.4 | 63.8 | — |

| Personal Income | Oct | 0.20% | 0.20% | 0.30% | 0.40% |

| Personal Spending | Oct | 0.20% | 0.20% | 0.70% | — |

| S&P CoreLogic CS 20-City YoY NSA | Sept | 3.90% | 3.92% | 2.16% | 2.14% |

Source: Bloomberg

Past performance is not indicative of future results. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Material presented has been derived from sources considered to be reliable and has not been independently verified by us or our personnel. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, other investments or to adopt any investment strategy or strategies. Investors must make their own decisions based on their specific investment objectives and financial circumstances. Investing involves risk, including loss of principal.

Clark Capital Management Group is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Clark Capital Management Group’s advisory services can be found in its Form ADV which is available upon request.

Fixed income securities are subject to certain risks including, but not limited to: interest rate (changes in interest rates may cause a decline in market value or an investment), credit, prepayment, call (some bonds allow the issuer to call a bond for redemption before it matures), and extension (principal repayments may not occur as quickly as anticipated, causing the expected maturity of a security to increase).

Clark Capital utilizes a proprietary investment model to assist with the construction of the strategy and to assist with making investment decisions. Investments selected using this process may perform differently than expected as a result of the factors used in the model, the weight placed on each factor, and changes from the factors’ historical trends. There is no guarantee that Clark Capital’s use of a model will result in effective investment decisions.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards and political and economic risks. These risks are enhanced in emerging market countries.

The value of investments, and the income from them, can go down as well as up and you may get back less than the amount invested.

Equity securities are subject to price fluctuation and possible loss of principal. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices. Certain investment strategies tend to increase the total risk of an investment (relative to the broader market). Strategies that concentrate their investments in limited sectors are more vulnerable to adverse market, economic, regulatory, political, or other developments affecting those sectors.

JOLTS is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

The Producer Price Index (PPI) program measures the average change over time in the selling prices received by domestic producers for their output. The prices included in the PPI are from the first commercial transaction for many products and some services.

References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time (each, an “index”) are provided for your information only. Reference to an index does not imply that the portfolio will achieve returns, volatility or other results similar to that index. The composition of the index may not reflect the manner in which a portfolio is constructed in relation to expected or achieved returns, portfolio guidelines, restrictions, sectors, correlations, concentrations, volatility or tracking error targets, all of which are subject to change. Investors cannot invest directly in an index.

The Bloomberg Barclays U.S. Municipal Index covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds.

The Bloomberg US Treasury Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury. Treasury bills are excluded by the maturity constraint, but are part of a separate Short Treasury Index.

The Dow Jones Industrial Average indicates the value of 30 large, publicly owned companies based in the United States.

The NASDAQ Composite is a stock market index of the common stocks and similar securities listed on the NASDAQ stock market.

The S&P 500 measures the performance of the 500 leading companies in leading industries of the U.S. economy, capturing 80% of U.S. equities.

The S&P 500® Equal Weight Index (EWI) is the equal-weight version of the widely-used S&P 500. The index includes the same constituents as the capitalization weighted S&P 500, but each company in the S&P 500 EWI is allocated a fixed weight – or 0.2% of the index total at each quarterly rebalance.

The University of Michigan Consumer Sentiment Index rates the relative level of current and future economic conditions. There are two versions of this data released two weeks apart, preliminary and revised. The preliminary data tends to have a greater impact. The reading is compiled from a survey of around 500 consumers.

The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 Index companies with lower price-to-book ratios and lower forecasted growth values.

The Russell 2000 Index is a small-cap stock market index that represents the bottom 2,000 stocks in the Russell 3000.

The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

The 10 Year Treasury Rate is the yield received for investing in a US government issued treasury security that has a maturity of 10 year. The 10 year treasury yield is included on the longer end of the yield curve. Many analysts will use the 10 year yield as the “risk free” rate when valuing the markets or an individual security.

The Bloomberg Barclays U.S. Corporate High-Yield Index covers the U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below.

The Bloomberg Barclays U.S. Credit Index measures the investment grade, U.S. dollar denominated, fixed-rate taxable corporate and government related bond markets.

The Bloomberg Aggregate Bond Index or “the Agg” is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

The 30-Year Treasury is a U.S. Treasury debt obligation that has a maturity of 30 years. The 30-year Treasury used to be the bellwether U.S. bond but now most consider the 10-year Treasury to be the benchmark.

The ISM Non-Manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms’ purchasing and supply executives, within 60 sectors across the nation, by the Institute of Supply Management (ISM). The ISM Non-Manufacturing Index tracks economic data, like the ISM Non-Manufacturing Business Activity Index. A composite diffusion index is created based on the data from these surveys, that monitors economic conditions of the nation.

ISM Manufacturing Index measures manufacturing activity based on a monthly survey, conducted by Institute for Supply Management (ISM), of purchasing managers at more than 300 manufacturing firms.

The MSCI Emerging Markets Index captures large and mid cap representation across 27 Emerging Markets (EM) countries.

The MSCI ACWI ex USA Index captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding the US) and 27 Emerging Markets (EM) countries*. With 2,359 constituents, the index covers approximately 85% of the global equity opportunity set outside the US

The S&P CoreLogic Case-Shiller 20-City Composite Home Price NSA Index seeks to measures the value of residential real estate in 20 major U.S. metropolitan areas. The U.S. Treasury index is based on the recent auctions of U.S. Treasury bills. Occasionally it is based on the U.S. Treasury’s daily yield curve.

The Consumer Price Index (CPI) measures the change in prices paid by consumers for goods and services. The CPI reflects spending patterns for each of two population groups: all urban consumers and urban wage earners and clerical workers.

In the United States, the Core Personal Consumption Expenditure Price (CPE) Index provides a measure of the prices paid by people for domestic purchases of goods and services, excluding the prices of food and energy.

The VIX Index is a calculation designed to produce a measure of constant, 30-day expected volatility of the U.S. stock market, derived from real-time, mid-quote prices of S&P 500® Index (SPX℠) call and put options. On a global basis, it is one of the most recognized measures of volatility — widely reported by financial media and closely followed by a variety of market participants as a daily market indicator.

The Conference Board’s Leading Indexes are the key elements in an analytic system designed to signal peaks and troughs in the business cycle. The leading, coincident, and lagging economic indexes are essentially composite averages of several individual leading, coincident, or lagging indicators. They are constructed to summarize and reveal common turning point patterns in economic data in a clearer and more convincing manner than any individual component – primarily because they smooth out some of the volatility of individual components.

Gross domestic product (GDP) is the standard measure of the value added created through the production of goods and services in a country during a certain period.

Index returns include the reinvestment of income and dividends. The returns for these unmanaged indexes do not include any transaction costs, management fees or other costs. It is not possible to make an investment directly in any index.

CCM-993

![]()